Photo courtesy of DuPont.

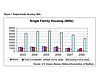

The historic downturn in residential construction continues, with areas that experienced the greatest appreciation seeing the greatest decline. In the last six months, the residential housing recession has fallen further than nearly anyone anticipated - ChemQuest included. As of January 2009, peak to trough prices have fallen 25%, with little indication that a floor has been set. Single-family building starts have fallen from an annual rate of 1.046 million at the end of 2007 to 625,000 near the end of 2008. The contagion from residential construction has now affected the rest of the economy, hence the worst residential construction recession in the post-World War II era, surpassing the residential downturn of 1978-1982.

Historically, residential housing has led the economy into and out of recessions. Look to an increase in new housing builds as a leading indicator that the recession is near an end. Unfortunately, there is little on the horizon to portend a correction in the near term. The ChemQuest Group has lowered its projected long-term volume growth rate for adhesive usage in construction from 3.2% to 0.7% through 2010. One reason that it isn’t negative is because construction outside of the residential sector has held up comparatively well.

Figure 1. Single-Family Housing, 000s

Non-Residential Spending

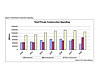

Despite the downturn in residential construction, non-residential construction spending appears to have increased in 2008, according to the U.S. Census Bureau. Construction markets showing a year-over-year increase include office, health care, power and manufacturing. Additional spending on public construction has also reduced the impact of the residential construction downturn and will continue under any fiscal stimulus package.The economic slowdown has also affected the residential remodeling market. Remodeling contains improvements and maintenance/repairs. The overall size of the remodeling market is about 1/5 the size of new residential construction. Of that, spending is traditionally split 80/20 in favor of improvements vs. maintenance. During the residential boom (2002-2006), many owners increased spending on large-sale remodeling projects, when low interest rates combined with increased equity in their homes helped fund them.

Although remodeling projects generally use less adhesive than new construction, they still represent an area of significant adhesive demand. Currently, homeowners continue to spend on maintenance but are no longer undertaking large improvements. The long-term trend of homeowners moving away from do-it-yourself (DIY) and hiring others for projects has also reversed in the current economic downturn. DIY has seen resurgence as homeowners seek to lower the costs of necessary repairs and smaller-scale projects by substituting personal labor for that of contractors. The result is a boost to consumer adhesive demand. The ChemQuest Group projects DIY to grow 4.4% through 2010.

Figure 2. Total Private Construction Spending

Going Forward

The increase in prices of single-family houses led to a rush of investment in residential construction. As recently as the end of 2005, new residential investment accounted for an unsustainable 6.5% of GDP. It is now at a historic low of less than 3% of GDP. Assuming a normal recovery from the current recession, look for a return to more stable residential-construction spending in the future, at or near 4.5% of GDP. As far as housing prices are concerned, they have averaged a multiple of 2.8 times household income but rose to a peak of 3.9 times income in 2005. In order to get back to 2.8, prices will have to fall another 15%.A. Todd Muhleman is manager of Strategic Planning for The ChemQuest Group Inc., an international strategic management consulting firm specializing in the adhesives, sealants and coatings industries headquartered in Cincinnati. For more information, phone (513) 469-7555 or visit www.chemquest.com.