Angela Austin of IAL Consultants, the firm that conducted the survey, commented, "During the past two years, the North American polyurethanes industry has balanced the reality of raw-material shortages and deteriorating production economics with growth in a number of product areas that impact quality of life. In the U.S., that growth has been stimulated by new products, such as viscoelastic foam and low-density rigid spray foams, as well as changes in consumer spending on such items as hardwood floors that require polyurethane coatings. Consumers have been purchasing larger refrigerators for their kitchens and additional units for other areas of the house, and larger vehicles - including minivans and SUVs - all of which use substantial amounts of polyurethane."

The results of the 2004 End Use Market Survey were released before the Polyurethanes 2005 Technical Conference and Trade Fair, which took place October 17-19, 2005. More than 1,450 attendees from 32 countries were in Houston to discuss polyurethane technology and trends.

Volume Up Across the Region

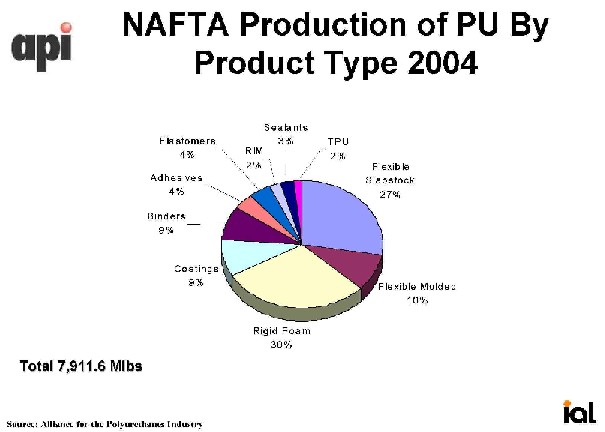

According to the survey, the North American polyurethanes industry volume for 2004 was 7,911.6 million pounds. Only Europe produced more than the NAFTA region in 2004, with 8,820 million pounds. In the United States, volume was 6,692.5 million pounds, up from 5,564 million pounds in 2002 and representing an annual 9.7% growth rate since 2002. Total U.S. production in 2004 was more than the total amount of polyurethane that was produced for the entire NAFTA region in 2002.Similar to survey results presented in 2002, growth was high in Canada, where production of polyurethane materials increased 10.7% between 2002 and 2004. During that period, Canadian polyurethane production totaled 720 million pounds, up from 588 million pounds in the 2000-2002 period. In addition, Canadian production accounted for 9% of the total NAFTA market.

Mexico volume was 499.1 million pounds and was bolstered by an increase in demand for Mexican raw materials. Many U.S. companies produce appliances, footwear, textiles, and furniture in Mexico for export, and this supported strong growth in domestic polyurethane production.

"Overall, the polyurethanes industry has continued to grow at a rate equal or greater than GDP across the NAFTA region," Austin said, "despite the maturity of its main end use industries - construction, refrigeration, automotive and furniture - in the U.S. and Canada."

"The results of the 2004 survey demonstrate the resilience of the polyurethanes industry," said Dick Mericle, executive director of the Alliance for the Polyurethanes Industry. "Our industry was able to weather the recent economic storm and now higher consumer demand is having a very positive effect on the growth of polyurethane production."

The report also showed that the top three polyurethane end-use applications remained unchanged from two years ago: construction, transportation, and furniture. Foam scrap and bedding rounded out the rest of the top five applications.

CASE

The use of polyurethane in coatings, adhesives and sealants formulations has experienced growth partly because of construction market dynamics. The market for construction has remained steady for both the residential and commercial sectors in the United States, creating a higher growth market for many polyurethane products. For example, the prevalence of hardwood floors that require polyurethane coatings has contributed to that growth. Also, a general consumer push toward increased comfort in everyday life has led automotive OEMs to seek improvements in vehicle stability through the use of polyurethane elastomers as shock absorbers.Production of polyurethane coatings totaled 712 million pounds in North America in 2004, up from 612 million pounds in 2002. Among coating types, waterborne polyurethane dispersions experienced the most demand. Adhesive and elastomers production both totaled approximately 316.5 million pounds in 2004, up from approximately 272 million pounds in 2002.

The End Use Market Survey, conducted every two years, addresses the current state of the North American polyurethanes industry. IAL Consultants interviewed more than 430 companies in North America, including end-users, formulators and producers, to complete the survey.

The End Use Market Survey was sponsored by the Alliance for the Polyurethanes Industry, a business unit of the American Plastics Council. For further information, contact Dick Mericle, Alliance for the Polyurethanes Industry, at (703) 741-5652 or visit www.polyurethane.org.

API promotes the sustainable growth of the polyurethane industry, in accordance with the principles of Responsible Care®, by identifying and managing issues that could impact the industry, in cooperation with user groups. Its 73 members are U.S. producers or distributors of chemicals and equipment used to make polyurethane or are manufacturers of polyurethane products.

API is a business unit of The American Plastics Council. APC advocates unlimited opportunities for plastics and promotes their economic, environmental and societal benefits.