Internal complexity issues can have an adverse impact on a company's profitability if they are not properly addressed.

It is not surprising that today’s business environment continues to become increasingly complex. Global economic interconnectivity, fast-paced communications and highly competitive pressures are only a few of the factors that companies deal with on a daily basis. It is well established that companies with a succinct strategic plan are best prepared to deal with-and ideally prosper from-this external complexity.

What is not typically evident, though, is the internal complexity that almost always arises in response and that then translates into inefficient and ineffective business processes. Unfortunately, it is here where companies are often ill-prepared (if not unprepared) to deal with hidden costs and the resultant drain on the company’s bottom line.

Sales and Pricing

The first area to scrutinize is sales. While the sales department seems like a convenient “whipping boy,” the matter is more complicated than questioning whether enough calls are being made. Competitive market pressures have created a trend toward greater product differentiation and customization.

On one level, customization is good if it ultimately increases sales volume and revenues. However, the resultant product line proliferation inevitably leads to increases in raw material and finished goods inventories, which have an associated cost that is not often realized and recovered. Therefore, the big question that should be asked is whether that increased volume was worth it and/or if the increased sales revenue was profitable. If the answer is no, then the organization needs to understand why.

More than likely, the customized products were not priced to the value that they bring to the end user. Pricing a custom product at the same level as a standard product is great for the customer, but it is not so great for the company’s bottom line. Understanding pricing-to-value and getting a handle on the myriad discounts that are frequently used in such transactions are useful ways to address profit “leaks” that yield lower-than-expected “pocket margins” (see Figure 1).

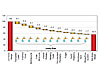

At the same time, companies need to analyze how they manage their customer base: not all customers are created equal (see Figure 2). In many cases, the 80:20 rule is ignored and companies operate at more like 90:10-meaning that small accounts receive the same treatment (pricing, discounts, service, etc.) as big accounts. Instead, pricing needs to reflect the value delivered. While pricing “allowances” may be made to large/strategic accounts, the same courtesies do not need to extend to smaller customers who do not warrant such considerations. Yet companies will too often sell a “C” product to a “C” customer at the same price and/or discount as an “A” customer and an “A” product-and then wonder why profits are not at expected levels. By exhibiting better pricing discipline, companies can identify where disparities exist and adjust prices to truly reflect the value delivered (see Figure 3).

Examining Research and Development

Another area that contributes significantly to internal complexity is R&D. Here, the issues tend to result from a misalignment between what products are being developed and whether they actually deliver the intended value to customers. Nothing is worse than developing a product that no one wants, that is not viewed as innovative and/or cannot be sold for a reasonable margin.

Better coordination with sales ensures that the R&D department is aware of what value needs to be delivered and whether customer needs have changed. Because both time and technical resources are finite in nature, companies that do not maximize their utility suffer a hidden hit to their bottom line. Conversely, efforts to further enhance coordination between R&D and sales yield more timely results that lead to capturing hidden value.

Managing Production

Finally, focus should obviously be put on production. Organizations frequently focus significant cost-cutting efforts on supply chain and manufacturing operations, but “trimming fat” rarely seems to cure the problem because it fails to recognize and address the root causes of the complexity that plagues them.

Through better analysis and management of customer and product tails, customers that cannot be profitably serviced are eliminated, and products that cannot be profitably sold can be dropped. This lessens the degree of complexity and allows manufacturers to optimize asset utilization and effectively manage inventories. In turn, these manufacturers have the ability to better handle small batches of customized products-without the customization process silently eating at the bottom line.

By understanding where internal complexities exist within a company, how they came into existence and what their adverse impact is on the bottom line, companies are better able to capture the hidden value-and EBITDA-that is there for the taking.

For more information, phone (513) 469-7555 or visit www.chemquest.com.