The slow recovery from the historic downturn in residential construction continues in 2016. In the mid-2000s, increasing prices and easy credit led to a rush of investment in residential construction. At the end of 2005, new residential investment accounted for an unsustainable 6.5% of GDP above its long-term rate. After dropping to a historic low of under 2.6% of GDP in 2010, it has since rebounded to 3.6%.

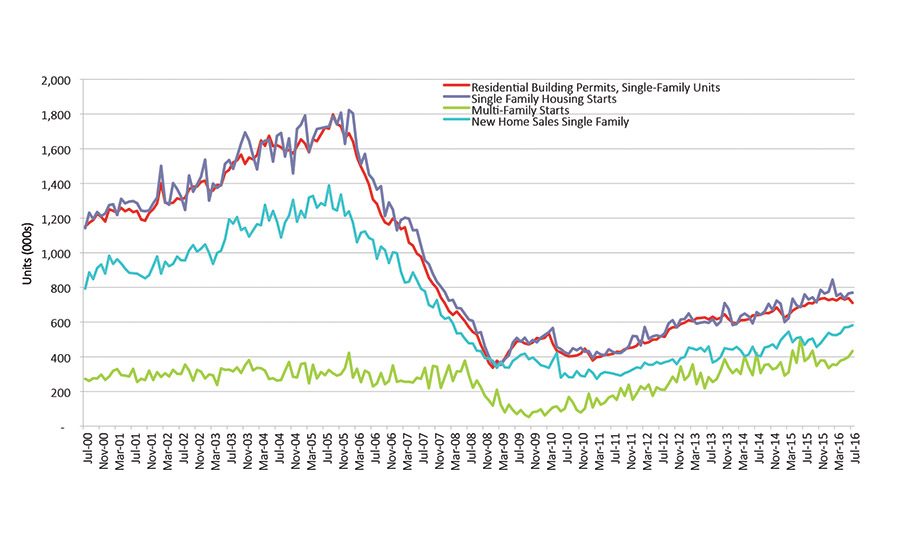

Both single- and multi-family housing starts have recovered from their lows of 550,000/year at the end of 2008 to 1.2 million currently. In 2015, existing home sales were 5.9% higher than 2014, with 5.25 million sold. New home sales were up even more, at 14.6% in 2015 with 500,000 units sold. Employment gains, record low interest rates and low inventory of existing homes for sale continue to be supportive of the new home market. However, as Figure 1 shows, new home sales and starts remain well below their 2005 peak.

Other factors are limiting buyers, including price appreciation (up 5.4% year over year as of July), low inventory and more stringent loan criteria. In addition, demographic changes among buyers are influencing the market.

Home ownership rates continue to decline; this is most evident in those under the age of 45. Currently, the number of Americans owning their own house is under 62.9%—the lowest level since the mid-1960s—and well down from the peak of 69% in 2005. Those under 45 owning homes now are about 7% lower than the historical norms. This demographic shift toward renting has implications as to the type of housing stock being produced, mainly an increase of multi-family units for rent, and is influencing the trend toward smaller new single-family homes.

The unemployment rate for the construction industry was 4.5% in July, slightly lower than the current overall rate of 4.9%. Labor costs for builders are climbing due to many skilled workers leaving during the extended downturn in construction, offsetting lower costs of raw materials.

Traditionally, new residential housing led the economy into recession and historically has been a leading sector out of past recessions as well. The current recovery has been different, as housing has recovered at a much slower pace than previous recoveries (along with most areas of the economy). In fact, the U.S. has not experienced real GDP growth of 3% since the recession.

Non-Residential Construction Spending

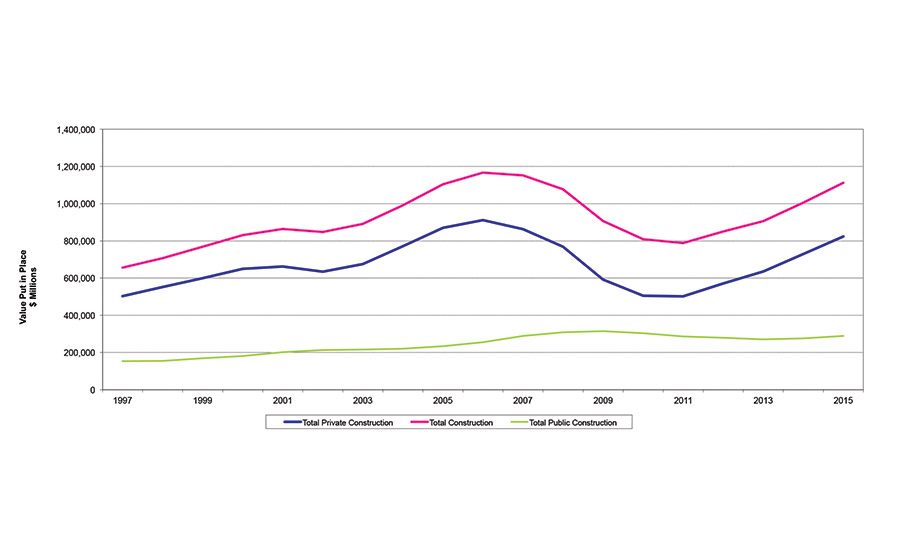

Non-residential construction spending continues to increase as well, up 8.4% in 2015, according to the U.S. Census Bureau. Construction markets showing double-digit year-over-year increases include lodging, office, amusement/recreation and communication. Private residential construction spending is 29.3% below its peak, while private non-residential construction spending is 4.8% below its peak. Public construction is 8.2% below its peak.

Residential Remodeling Market Continues to Flourish

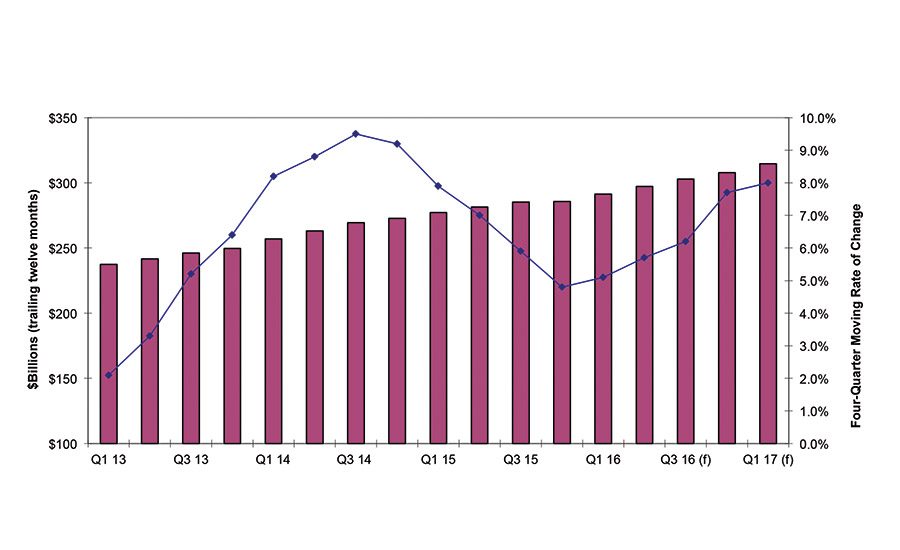

Remodeling includes both improvements and maintenance and repairs. Historically, spending is traditionally split 80/20 in favor of improvements vs. maintenance. Although remodeling projects use less adhesive than new construction, it is still an area of significant adhesive demand.

Currently, many homeowners are spending on improvements instead of upgrading to a larger residence. For the last two years, spending on remodeling has been growing about 10% per year. The long-term trend of homeowners moving away from do-it-yourself (DIY) and hiring others for projects has resumed after reversing a bit during the recession. ASI

A. Todd Muhleman is senior consultant for The ChemQuest Group Inc. For more information, phone (513) 469-7555 or visit www.chemquest.com.

Any views or opinions expressed in this column are those of the author and do not represent those of ASI, its staff, Editorial Advisory Board or BNP Media.