STRATEGIC SOLUTIONS: Macroeconomic and Sector Trends Affecting Adhesives

When

a billion isn’t a billion.

Adhesives are used extensively in manufacturing and

construction applications, filling a unique space in the economic value chain.

Although adhesives and sealants generally make up a very small percentage of a

final product’s cost, they are crucial to its function. Adhesive failure often

leads to product failure and expensive liabilities for a manufacturer. It is

the adhesives’ and sealants’ quality throughout production that makes

estimating short-term fluctuations in demand difficult.

Adhesives are used extensively in manufacturing and

construction applications, filling a unique space in the economic value chain.

Although adhesives and sealants generally make up a very small percentage of a

final product’s cost, they are crucial to its function. Adhesive failure often

leads to product failure and expensive liabilities for a manufacturer. It is

the adhesives’ and sealants’ quality throughout production that makes

estimating short-term fluctuations in demand difficult.

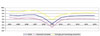

While we at ChemQuest are currently updating our global adhesives reports with projected growth trends for the next five-year period, we are simultaneously compiling our annual outlook for the adhesives, sealants and coatings industries. The first step in that process is determining what macroeconomic changes are affecting regional economies and end-use demand.

By the end of 2009, the global economy had finally emerged from its worst economic recession since World War II. The synchronized economic downturn in 2008 is being followed by positive GDP growth throughout nearly all economies, albeit at vastly different rates. Figure 1 shows the abrupt downturn in both advanced and emerging economies from 2008-2009 and the expectation of continued growth, though at slightly lower rates. China and India were able to avoid year-over-year declines in their GDP in 2009 and, along with Brazil, are poised for the strongest growth rates in 2010. The recovery in Europe is the most sluggish, barely emerging with positive growth at the end of 2009.

The United States is in the middle, with positive GDP growth rates heading into 2010. As of press time, the Q4 2009 annualized GDP is expected to be 4.5% for the U.S., but there are worries about the sustainability of future growth. Much of the rebound in growth is attributable to inventory adjustments, as firms restock inventory that was liquidated during the downturn. Another factor adding to GDP growth is the large amount of government spending, which is expected to decrease in the second half of 2010.

Other, less-positive factors in future GDP are the continued struggles in residential and commercial construction. Total U.S. construction in 2009 was down 15% compared to 2008. However, while new-home sales appear to have bottomed out in January 2009, they have yet to break out from the bottom. With uncertainty surrounding the labor market, and the Federal Reserve expected to end its support for the mortgage bond market, it is unlikely that construction will substantially rebound in 2010, but it is not expected to deteriorate further.

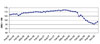

As shown in Figures 2a-b, capacity usage and industrial

production have both recovered from their recessionary lows. Capacity usage

reached a record low since our global adhesives reports series began in 1972.

As shown in Figures 2a-b, capacity usage and industrial

production have both recovered from their recessionary lows. Capacity usage

reached a record low since our global adhesives reports series began in 1972.

“Cash for Clunkers” helped U.S.

motor-vehicle sales surge to a seasonally adjusted annual rate (SAAR) of 14.1 million in August - only to drop off to

less than 10 million after the government program ended. Before the crisis,

annual sales in the U.S.

market had been >15 million since 2000. The question is: What number will

this be going forward? Our best guess is about 12 million units in 2010 and 14

million in 2011, which represents a CAGR of 17%. As for adhesives themselves,

ChemQuest estimates overall volume declines of 20% peak-to-trough for the

recession.

“Cash for Clunkers” helped U.S.

motor-vehicle sales surge to a seasonally adjusted annual rate (SAAR) of 14.1 million in August - only to drop off to

less than 10 million after the government program ended. Before the crisis,

annual sales in the U.S.

market had been >15 million since 2000. The question is: What number will

this be going forward? Our best guess is about 12 million units in 2010 and 14

million in 2011, which represents a CAGR of 17%. As for adhesives themselves,

ChemQuest estimates overall volume declines of 20% peak-to-trough for the

recession.

On a lighter note, readers may be surprised to learn that

more than one large-scale numbering system is used in the world. The two most

widely used are the long scale and the short scale; it can create confusion if

persons are referring to a large number using different systems. In fact, it

was during a conference call with a Dutch firm that I became aware of this

variance. America

and most other English-speaking nations use the short-scale numbering system

when referring to large numbers, while continental European nations continue to

use the long-scale system. Until it changed in 1974, the United Kingdom also used the long

scale.

On a lighter note, readers may be surprised to learn that

more than one large-scale numbering system is used in the world. The two most

widely used are the long scale and the short scale; it can create confusion if

persons are referring to a large number using different systems. In fact, it

was during a conference call with a Dutch firm that I became aware of this

variance. America

and most other English-speaking nations use the short-scale numbering system

when referring to large numbers, while continental European nations continue to

use the long-scale system. Until it changed in 1974, the United Kingdom also used the long

scale.

The Table shows where the two systems diverge, beginning

with a “billion.” Because of the possibility of a misunderstanding, it’s a good

idea to clarify the meaning of these numbers in international conversations

when they come up.

The Table shows where the two systems diverge, beginning

with a “billion.” Because of the possibility of a misunderstanding, it’s a good

idea to clarify the meaning of these numbers in international conversations

when they come up.

For more information, phone (513) 469-7555 or visit www.chemquest.com.

Source of Figure 1: IMF

Source of Figures 2a, 2b and 3: Federal Reserve

"Cash for Clunkers" helped U.S. motor vehicle sales surge.

Figure 1. Global GDP Growth (Annual % Change)

While we at ChemQuest are currently updating our global adhesives reports with projected growth trends for the next five-year period, we are simultaneously compiling our annual outlook for the adhesives, sealants and coatings industries. The first step in that process is determining what macroeconomic changes are affecting regional economies and end-use demand.

By the end of 2009, the global economy had finally emerged from its worst economic recession since World War II. The synchronized economic downturn in 2008 is being followed by positive GDP growth throughout nearly all economies, albeit at vastly different rates. Figure 1 shows the abrupt downturn in both advanced and emerging economies from 2008-2009 and the expectation of continued growth, though at slightly lower rates. China and India were able to avoid year-over-year declines in their GDP in 2009 and, along with Brazil, are poised for the strongest growth rates in 2010. The recovery in Europe is the most sluggish, barely emerging with positive growth at the end of 2009.

The United States is in the middle, with positive GDP growth rates heading into 2010. As of press time, the Q4 2009 annualized GDP is expected to be 4.5% for the U.S., but there are worries about the sustainability of future growth. Much of the rebound in growth is attributable to inventory adjustments, as firms restock inventory that was liquidated during the downturn. Another factor adding to GDP growth is the large amount of government spending, which is expected to decrease in the second half of 2010.

Other, less-positive factors in future GDP are the continued struggles in residential and commercial construction. Total U.S. construction in 2009 was down 15% compared to 2008. However, while new-home sales appear to have bottomed out in January 2009, they have yet to break out from the bottom. With uncertainty surrounding the labor market, and the Federal Reserve expected to end its support for the mortgage bond market, it is unlikely that construction will substantially rebound in 2010, but it is not expected to deteriorate further.

Figure 2a. Capacity Utilization - Manufacturing

Figure 2b. Industrial Production Index (seasonally adjusted)

Figure 3. U.S. Lightweight Auto/Truck Sales (SAAR) (million of units)

Table.

For more information, phone (513) 469-7555 or visit www.chemquest.com.

Source of Figure 1: IMF

Source of Figures 2a, 2b and 3: Federal Reserve

Links

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!