MARKET TRENDS: Labels in the Lead

U.S.

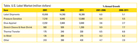

label shipments to reach $18.3 billion in 2011.

U.S. label shipments are

forecast to increase 5.1% annually to $18.3 billion in 2011. The best

opportunities are anticipated for the pressure-sensitive segment, which

accounts for the majority of label shipments. Pressure sensitives will face

increased competition from other application methods, such as stretch sleeve

and heat-shrink labels, which will post more rapid advances. Gains in the

stretch and shrink segment will be driven by increased use in the large

beverage packaging industry. Advances in resin technologies will also support

growth. These and other trends are presented in Labels, a

new study from The Freedonia Group Inc., a Cleveland-based industry research

firm.

U.S. label shipments are

forecast to increase 5.1% annually to $18.3 billion in 2011. The best

opportunities are anticipated for the pressure-sensitive segment, which

accounts for the majority of label shipments. Pressure sensitives will face

increased competition from other application methods, such as stretch sleeve

and heat-shrink labels, which will post more rapid advances. Gains in the

stretch and shrink segment will be driven by increased use in the large

beverage packaging industry. Advances in resin technologies will also support

growth. These and other trends are presented in Labels, a

new study from The Freedonia Group Inc., a Cleveland-based industry research

firm.

Paper will continue to dominate the label industry, but will slowly lose market share as the use of plastic stock materials expands rapidly. Advances will be based on the aesthetic and performance advantages of plastic labels; the growing use of plastic packaging; and the popularity of labeling methods that rely heavily on plastic substrates. Oriented polypropylene will exhibit the fastest growth among the major label resins, further supplanting polyvinyl chloride.

Primary packaging will remain the major market for labels through 2011, although labels used in secondary applications will post the fastest gains overall. A growing interest in the use of labels as a tool to create a strong brand identity will provide favorable opportunities for labels in the primary packaging industry, as will a rising interest in labels as a means of serving value-added functions such as enhancing security and providing expanded product information. Going forward, secondary labeling will benefit from continued demand for bar coding labels; the utilization of radio frequency identification (RFID); and electronic article surveillance (EAS).

Most of U.S. label shipments are comprised of labels printed in some manner before sale to the final user. Flexography, which will experience above-average advances through 2011, represents the most commonly used label printing method. A number of other printing techniques are also employed, including lithographic, screen, letterpress, gravure and digital. These processes are commonly combined in the label industry. Digital technology, for instance, will be increasingly incorporated with conventional techniques. Digitally printed label shipments will continue to expand at double-digit pace through 2011, aided by a growing trend toward the use of mass customization.

For more information, contact Corinne Gangloff, The Freedonia Group Inc., 767 Beta Drive, Cleveland, OH 44143-2326; phone (440) 684-9600; fax (440) 646-0484; e-mail pr@freedoniagroup.com; or visit www.freedoniagroup.com.

Photo: The Coca-Cola Co.

Paper will continue to dominate the label industry, but will slowly lose market share as the use of plastic stock materials expands rapidly. Advances will be based on the aesthetic and performance advantages of plastic labels; the growing use of plastic packaging; and the popularity of labeling methods that rely heavily on plastic substrates. Oriented polypropylene will exhibit the fastest growth among the major label resins, further supplanting polyvinyl chloride.

Primary packaging will remain the major market for labels through 2011, although labels used in secondary applications will post the fastest gains overall. A growing interest in the use of labels as a tool to create a strong brand identity will provide favorable opportunities for labels in the primary packaging industry, as will a rising interest in labels as a means of serving value-added functions such as enhancing security and providing expanded product information. Going forward, secondary labeling will benefit from continued demand for bar coding labels; the utilization of radio frequency identification (RFID); and electronic article surveillance (EAS).

Most of U.S. label shipments are comprised of labels printed in some manner before sale to the final user. Flexography, which will experience above-average advances through 2011, represents the most commonly used label printing method. A number of other printing techniques are also employed, including lithographic, screen, letterpress, gravure and digital. These processes are commonly combined in the label industry. Digital technology, for instance, will be increasingly incorporated with conventional techniques. Digitally printed label shipments will continue to expand at double-digit pace through 2011, aided by a growing trend toward the use of mass customization.

For more information, contact Corinne Gangloff, The Freedonia Group Inc., 767 Beta Drive, Cleveland, OH 44143-2326; phone (440) 684-9600; fax (440) 646-0484; e-mail pr@freedoniagroup.com; or visit www.freedoniagroup.com.

Links

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!