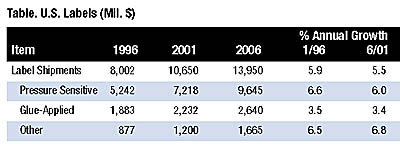

Market Trends U.S. Label Shipments to Grow Nearly 5% Through 2006

Technologies ranging from reduced space and two-dimensional bar coding to plateless digital printing will open a range of new labeling applications. Advances in label substrates, adhesives and coatings will also be important in this regard. Preventing even faster growth will be a cooling U.S. economy and maturity in key label applications. Competition from direct labelless printing will also hold down gains in applications such as mailing, primary packaging and corrugated box labeling.

These and other trends are presented in Labels, a new study from The Freedonia Group Inc., a Cleveland-based industrial market research firm. While paper will remain the leading label stock, plastics will continue to make inroads. Advances will be based on the aesthetic and performance advantages of plastic labels; the growing use of plastic packaging; and the popularity of labeling methods such as pressure-sensitive, in-mold and shrink, which rely heavily on plastic substrates. Oriented polypropylene will exhibit the fastest growth among the major label resins, further supplanting polyvinyl chloride. Paper labels, however, will be adversely affected by changes in the U.S. packaging mix, which will negatively impact metal cans and glass containers.

Pressure-sensitive adhesive (PSA) labels will remain the dominant type, accounting for over two-thirds of total output. Relatively novel, fast-growing, value-added applications such as color-printed variable information labels, expanded content labels in the medical and personal care markets, and labels used in conjunction with electronic security systems all rely on PSA application methods. As cost and speed differentials decline, PSA labels will also capture share from traditional wet-glue, gummed and heat-seal labels in packaging applications. In addition, PSAs retain essentially uncontested control of the information processing, secondary, office and consumer label markets, most of which are enjoying healthy secular growth.

Flexography will remain the primary label printing method, with above-average gains - especially for ultraviolet flexography - supported by flexo's low cost and the ongoing development of high quality, environmentally friendly UV-curing inks. Greater use of combination printing presses is also expected. In addition, label printing will continue to be revolutionized by advances in digital technologies ranging from dedicated digital label presses to the digitalization of conventional label printing methods.

For more information:

Labels is available for $3,900 from the Freedonia Group Inc., 767 Beta Drive, Cleveland, OH 44143. For more information, contact Corinne Gangloff, phone 440-684-9600; fax 440-646-0484; e-mail mailto:pr@freedoniagroup.com; or visit www.freedoniagroup.com.Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!