STRATEGIC SOLUTIONS: Global Pressure-Sensitive Materials Forecast

Regulatory pressure will continue to create opportunities for environmentally friendly alternatives.

It is estimated that the global pressure-sensitive materials industry will consume 47,271 million square meters in 2010 and experience 5% average annual growth rates for the next five years. The Asia Pacific region has emerged as the largest producer of pressure-sensitive materials; the region accounts for 47% of global production, primarily due to China’s emergence as a low-cost producer and major exporter of commodity tapes.

It is estimated that the global pressure-sensitive materials industry will consume 47,271 million square meters in 2010 and experience 5% average annual growth rates for the next five years. The Asia Pacific region has emerged as the largest producer of pressure-sensitive materials; the region accounts for 47% of global production, primarily due to China’s emergence as a low-cost producer and major exporter of commodity tapes.

Tape production accounted for 66% of all pressure-sensitive materials, while labels and graphics made up 28% and 6%, respectively (see Figure 1). In turn, the demand for pressure-sensitive adhesives (PSAs) reached $2.4 billion globally on the merchant market. This does not reflect captive production of adhesives by tape and label producers, which would add an additional 40-50% to the total.

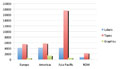

The regional breakdown of merchant adhesives production shown in Figure 2 illustrates the emerging dominance of Asia Pacific’s producers, as they garnered 54% of the global demand. The Americas and Europe (EU 27) attained 22% and 21%, respectively, of the market share.

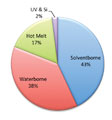

Not too surprisingly, solventborne technologies maintained their dominance with 43% share of merchant PSAs (see Figure 3). Waterborne (38%) and hot-melt (17%) technologies continued their march toward offering environmentally friendly solutions, but specialty applications remained squarely in the corner of solventborne technologies. Radiation-curing UV technologies and silicone PSAs for specialty applications (e.g., medical and electronics) made up the balance of total demand (2%).

Not too surprisingly, solventborne technologies maintained their dominance with 43% share of merchant PSAs (see Figure 3). Waterborne (38%) and hot-melt (17%) technologies continued their march toward offering environmentally friendly solutions, but specialty applications remained squarely in the corner of solventborne technologies. Radiation-curing UV technologies and silicone PSAs for specialty applications (e.g., medical and electronics) made up the balance of total demand (2%).

Regulatory pressure will undoubtedly continue to create opportunities for environmentally friendly alternatives. Japan is reportedly promulgating two laws, which would create “black swan” opportunities for pressure-sensitive materials and adhesives producers by the end of the decade. The first will require the industry to lower volatile organic compound (VOC) limits to less than 120 parts per million, while the second is related to post-consumer recycling and will require producers of consumer goods-from autos to electronics-to disassemble and recycle their components.

Figure 1. Pressure-Sensitive Material Production

Figure 2. PSA Production by Region

Tape production accounted for 66% of all pressure-sensitive materials, while labels and graphics made up 28% and 6%, respectively (see Figure 1). In turn, the demand for pressure-sensitive adhesives (PSAs) reached $2.4 billion globally on the merchant market. This does not reflect captive production of adhesives by tape and label producers, which would add an additional 40-50% to the total.

The regional breakdown of merchant adhesives production shown in Figure 2 illustrates the emerging dominance of Asia Pacific’s producers, as they garnered 54% of the global demand. The Americas and Europe (EU 27) attained 22% and 21%, respectively, of the market share.

Figure 3. PSA Production by Market

Regulatory pressure will undoubtedly continue to create opportunities for environmentally friendly alternatives. Japan is reportedly promulgating two laws, which would create “black swan” opportunities for pressure-sensitive materials and adhesives producers by the end of the decade. The first will require the industry to lower volatile organic compound (VOC) limits to less than 120 parts per million, while the second is related to post-consumer recycling and will require producers of consumer goods-from autos to electronics-to disassemble and recycle their components.

Links

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!