STRATEGIC SOLUTIONS: Macro Economic Environment

“If something cannot go on forever, it will stop.” -Herbert Stein

Although the Federal Reserve Board has ended most of the extraordinary liquidity facilities put in place after the collapse of Lehman Brothers in September 2008, the current policy of “quantitative easing” is setting the stage for another round of global commodity inflation. Even more worrisome than rising commodity prices is the recognition that many of the conditions that paved the foundation for the crisis are still in place more than two years later.

The global trade imbalances leading into the crisis of 2008 have not been addressed on a cooperative basis. Instead, neo-mercantilism continues to flourish. Nations continue to keep or expand trade advantages by manipulating their currencies to maximize their trade surplus or ameliorate their trade deficit rather than letting the market rebalance exchange rates to correct these imbalances. In addition, the “too big to fail” banks and government-sponsored enterprises (GSEs), including Fannie Mae, that were bailed out during the crisis have created a moral hazard where these large firms are still implicitly encouraged to make risky bets knowing that they can keep the gains and socialize the losses should they occur.

Europe’s sovereign debt crisis, which began in Greece and continued on to Ireland and Portugal, also threatens the stability of the global economy unless the European Union (EU) can agree on a large enough solution to get ahead of the next member’s fiscal crisis. Ben Bernanke and the Fed have embarked on a course of action to devalue the dollar, putting pressure on China to end its fixed exchange rate with the dollar or face domestic inflation caused by linking their monetary policy to that of the Fed. All of these policy decisions, as well as the dramatic post-crisis increase in global sovereign indebtedness, increase the likelihood that the next global crisis will be even deeper and more difficult to recover from.

Despite these concerns, economists and the public have an increasingly positive outlook for the global economy as time passes without another crisis event; they are hopeful that growth will be enough to be self-sustaining once government stimulus is withdrawn. In the U.S., the two-year extension of the Bush-era tax cuts look to add an additional 1% to GDP in 2011, moving the consensus real growth rate among economists from 2.5% to 3.5% for the year.

In addition to unit volume growth, the transportation industry is moving toward a much greater use of lightweight composite materials. While the Boeing 787 Dreamliner has been beset with numerous delays because of its ground-breaking construction, the fuel savings that these “weight-saving” technologies bring are being seriously considered in the automotive sector. These materials use structural adhesives instead of steel and aluminum with welding and mechanical fasteners, but will need to substantially come down in price to become a competitive alternative to traditional construction methods. A primary driver is the 2020 CAFE standards that mandate an average of 35 mpg, 40% higher than today’s vehicles, something that will require revolutionary re-engineering to meet.

For more information, phone (513) 469-7555 or visit www.chemquest.com.

Although the Federal Reserve Board has ended most of the extraordinary liquidity facilities put in place after the collapse of Lehman Brothers in September 2008, the current policy of “quantitative easing” is setting the stage for another round of global commodity inflation. Even more worrisome than rising commodity prices is the recognition that many of the conditions that paved the foundation for the crisis are still in place more than two years later.

The global trade imbalances leading into the crisis of 2008 have not been addressed on a cooperative basis. Instead, neo-mercantilism continues to flourish. Nations continue to keep or expand trade advantages by manipulating their currencies to maximize their trade surplus or ameliorate their trade deficit rather than letting the market rebalance exchange rates to correct these imbalances. In addition, the “too big to fail” banks and government-sponsored enterprises (GSEs), including Fannie Mae, that were bailed out during the crisis have created a moral hazard where these large firms are still implicitly encouraged to make risky bets knowing that they can keep the gains and socialize the losses should they occur.

Europe’s sovereign debt crisis, which began in Greece and continued on to Ireland and Portugal, also threatens the stability of the global economy unless the European Union (EU) can agree on a large enough solution to get ahead of the next member’s fiscal crisis. Ben Bernanke and the Fed have embarked on a course of action to devalue the dollar, putting pressure on China to end its fixed exchange rate with the dollar or face domestic inflation caused by linking their monetary policy to that of the Fed. All of these policy decisions, as well as the dramatic post-crisis increase in global sovereign indebtedness, increase the likelihood that the next global crisis will be even deeper and more difficult to recover from.

Despite these concerns, economists and the public have an increasingly positive outlook for the global economy as time passes without another crisis event; they are hopeful that growth will be enough to be self-sustaining once government stimulus is withdrawn. In the U.S., the two-year extension of the Bush-era tax cuts look to add an additional 1% to GDP in 2011, moving the consensus real growth rate among economists from 2.5% to 3.5% for the year.

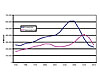

Figure 1. U.S. Lightweight Auto/Truck Sales (SAAR, millions of units)

Implications for the Adhesives Industry

The adhesives industry has seen firms at all levels of the value chain move to streamline operations through reduced capacity, staffing and inventory since the crisis. The largest benefactors have been raw material and intermediate product producers that have been able to pass along their cost increases to the formulators through capacity cutbacks, which have also been affected by unforeseen events such as force majeure outages in the acrylics supply chain. Acrylics are not the exception; nearly all chemistries for adhesive formulation continue to see substantive price increases.Transportation

Annual light truck and auto sales in the U.S. market averaged > 15 million from 2000 to 2008, but fell to 10.4 million in 2009. Since the initial downturn after the end of the “cash for clunkers” program, the industry has been steadily growing, selling 11.5 million units in 2010, with the final quarter of 2010 averaging more than 12 million units on a seasonally adjusted annual rate (SAAR). The 2012 consensus forecast from the industry is for 12.5 million units, a year-over-year increase of 11%.In addition to unit volume growth, the transportation industry is moving toward a much greater use of lightweight composite materials. While the Boeing 787 Dreamliner has been beset with numerous delays because of its ground-breaking construction, the fuel savings that these “weight-saving” technologies bring are being seriously considered in the automotive sector. These materials use structural adhesives instead of steel and aluminum with welding and mechanical fasteners, but will need to substantially come down in price to become a competitive alternative to traditional construction methods. A primary driver is the 2020 CAFE standards that mandate an average of 35 mpg, 40% higher than today’s vehicles, something that will require revolutionary re-engineering to meet.

Figure 2. Private Construction Spending

Construction

Private construction spending in the U.S. continues to lag the rest of the economy. Efforts to revive the residential housing market have met with lukewarm success, at best. Since the end of the last round of homebuyer incentives, prices have begun to decline again across nearly all markets, and the market appears to be setting up for a double dip. Despite the continuing problems, residential investment (mainly new single and multi-family units, as well as home improvements) looks to have finally bottomed and may add to GDP growth in 2011 for the first time since 2005.Global Growth

A number of issues stand ready to derail global growth in 2011 or later years. Hopefully, however, 2011 can build on the positive growth of 2010. The consensus outlook for GDP growth in the global economy for 2011 is a robust 4-4.5%, down slightly from 2010’s rate of 4.8% forecast by the International Monetary Fund.About the Author

A. Todd Muhleman is manager of Strategic Planning for The ChemQuest Group Inc., an international strategic management consulting firm specializing in the adhesives, sealants and coatings industries headquartered in Cincinnati.For more information, phone (513) 469-7555 or visit www.chemquest.com.

Links

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!